Merchant account vs payment processor for high-risk businesses.

Navigate the complex landscape of payment processing for high-risk businesses and learn about various roles like merchant accounts and payment facilitators.

21+

Years of Experience

500+

Successful Partnerships

99%

Client Satisfaction

100+

Industries Served

When running a high-risk business, understanding the distinctions between a merchant account and a payment processor is crucial. These terms are often used interchangeably, but they refer to different aspects of handling financial transactions.

What is a Merchant Account?

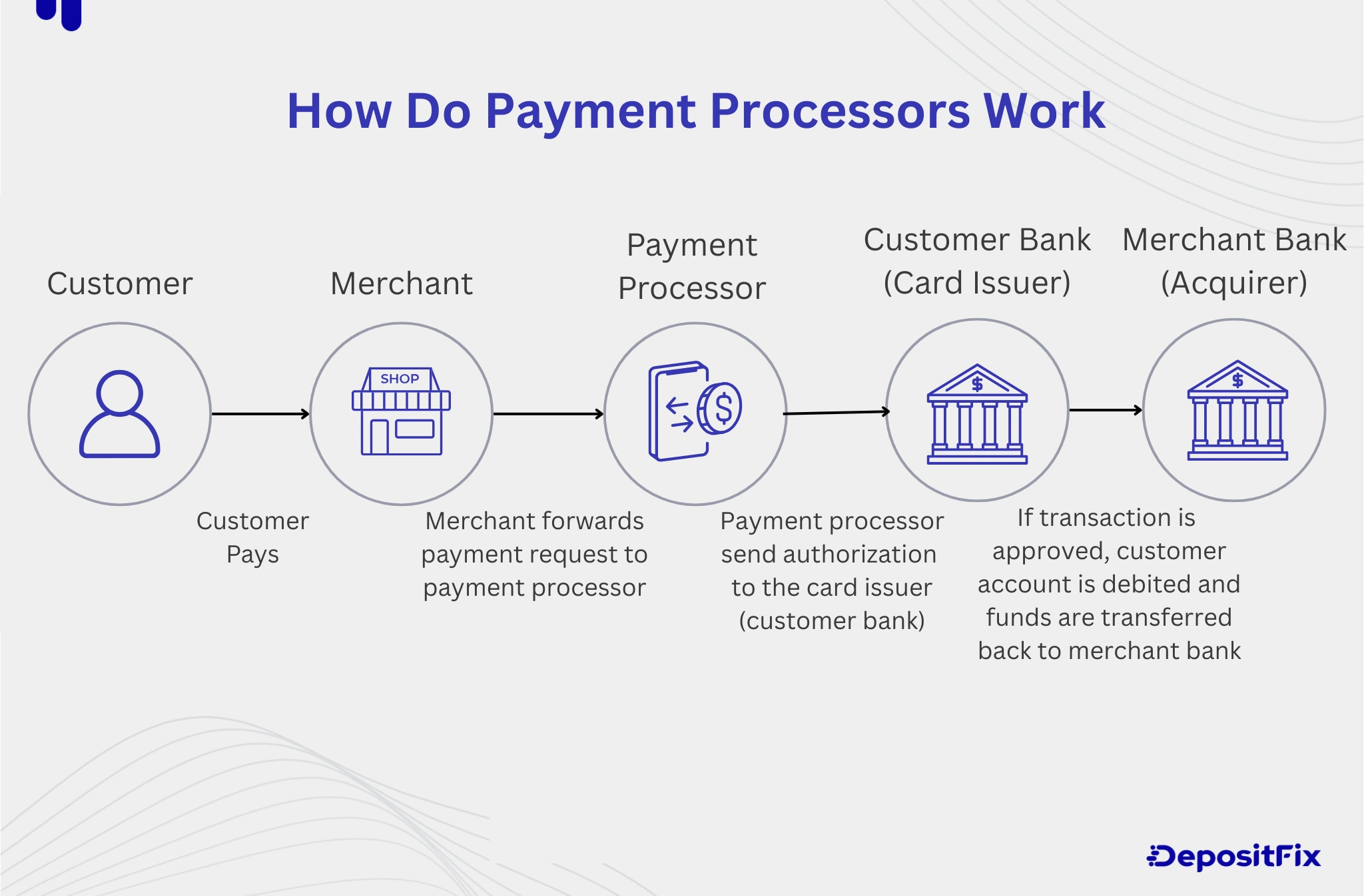

A merchant account is a specialized bank account that allows a business to accept payments from a variety of payment methods, primarily credit and debit cards. This account acts as a bridge between a customer’s bank and a business’s bank.

What is a Payment Processor?

A payment processor facilitates the transaction process. It manages the transfer of data between the merchant account and the customer’s credit card or other payment methods used.

Payment Gateway Explained

A payment gateway is software that captures and transfers payment data from a customer to the payment processor. It essentially serves as the interface that bridges the merchant’s website with the payment processor.

Understanding ISO

An Independent Sales Organization (ISO) is a company that has been contracted by a merchant account provider to service or provide merchant accounts for businesses.

The Role of Acquirers

Acquirers are financial institutions that process credit and debit card payments on behalf of a merchant. This might be a bank or financial institution that is partnered with the merchant.

What is an Aggregator?

An aggregator allows merchants to accept payments under a single umbrella without needing to establish their own merchant account. This is typically a popular option for smaller businesses.

Defining Payment Facilitators

A payment facilitator is a service provider that allows businesses to facilitate payments in a more streamlined manner, often being a solution for businesses that may struggle to get approved for a normal merchant account.

Why High-Risk Businesses Need Direct Underwriting

High-risk businesses face unique challenges that require tailored solutions. Unlike standard businesses, high-risk merchants often experience higher transaction fees and might be subject to stricter regulations. Hence, obtaining direct underwriting from a financial institution is essential to reflect individual risk profiles properly.

Conclusion

Understanding the differences between a merchant account, payment processor, and various facilitators can position high-risk businesses for greater success. While aggregators may seem appealing due to ease of entry, direct underwriting often provides a more sustainable solution for long-term growth.

Why Trust High Wire Payments?

Your partner in high-risk payment solutions.

Experience

We offer over 20 years of expertise in high-risk payment processing.

Tailored Services

Our services are specifically designed for high-risk industries.

Client Support

Dedicated support to help you every step of the way.

What is the fee structure for high-risk merchants?

Fees vary based on the type of business, transaction volume, and risk.

How can I apply for a merchant account?

You can apply through our website for a quick and easy approval process.

What makes a business high-risk?

Certain industries, high transaction volumes, and previous chargebacks contribute to the high-risk classification.

Can I switch processors easily?

Yes, but it’s essential to ensure no service interruptions occur during the switch.

What documentation is needed for application?

Typically, you need to provide financial statements, business registration documents, and identification.

Ready to Get Your Business Started?

Let High Wire Payments guide you through the payment processing maze with expertise and tailored solutions.

Apply Now →