Chargeback reason codes explained.

This article covers everything you need to know about chargeback reason codes, why they matter, and how to respond effectively.

What Are Chargeback Reason Codes?

Chargeback reason codes are essential tools for card networks and merchants alike that categorize the reason behind a cardholder’s dispute regarding a transaction. This categorization plays a vital role in the processing of disputes and helps in identifying patterns and trends in chargebacks.

Why Chargeback Reason Codes Matter

These codes are crucial for merchants to understand effective management of disputes. Chargeback reason codes can directly impact a merchant’s bottom line, as higher chargeback rates can lead to increased fees, fines, and even termination of merchant accounts.

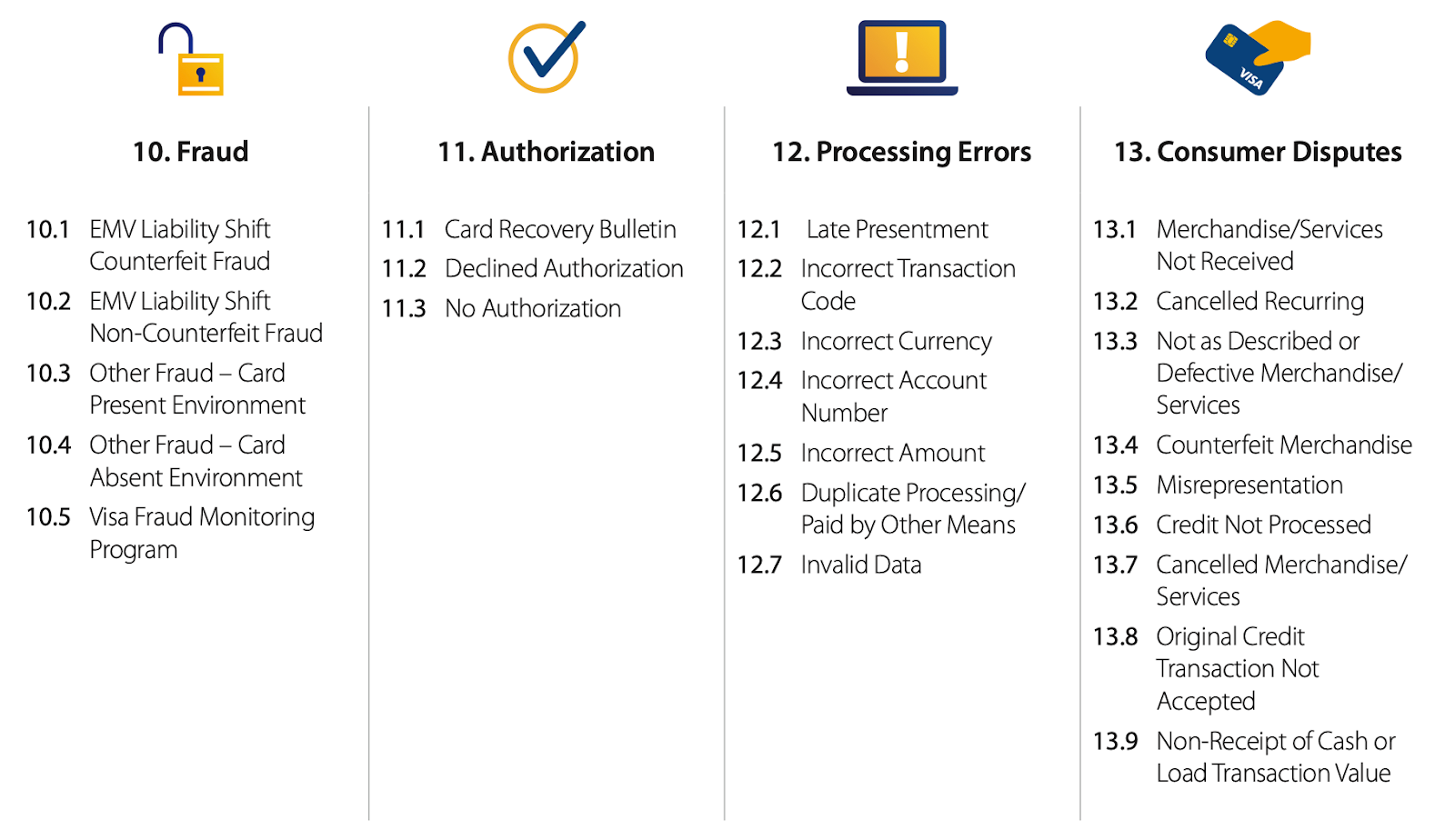

Common Categories of Chargeback Reason Codes

Chargeback reason codes typically fall into various categories, each specifying the type of dispute. Here we discuss some common categories:

- Fraud: This category includes unauthorized transactions, where the cardholder did not authorize the charge.

- Authorization: These involve disputes related to a lack of prior approval or incorrect transaction amounts.

- Processing errors: Errors that occur during transaction processing lead to disputes, often relating to incorrect charges.

- Product not received: Customers may dispute charges if they believe their purchases never arrived.

- Product unacceptable: If the item received does not match the description or is damaged, customers may file a chargeback.

- Credit not processed: Disputes arise when expected refunds or credits have not been processed or received by the customer.

- Subscription cancellation: Customers may dispute charges for subscriptions they canceled prior to the billing date.

- Duplicate billing: This occurs when the same transaction is charged multiple times in error.

Understanding Card Network Codes

It’s essential to note that each card network, such as Visa, Mastercard, American Express, and Discover, uses its own set of reason codes. Merchants need to review the actual dispute notice associated with each chargeback to understand the specific reason code and properly respond to the dispute.

Evidence Examples for Chargeback Disputes

When responding to chargebacks, merchants should gather and present pertinent evidence. Some examples of useful evidence include:

- Shipping receipts and tracking information for claims of products not received.

- Email correspondence that shows customer acknowledgment of service or product acceptance.

- Transaction records showing the authorization process.

- Records of communication regarding subscription cancellations and the agreed terms.

Prevention Tips for Chargebacks

It’s essential to implement strategies to reduce chargebacks:

- Use clear product descriptions and photographs to avoid misunderstandings.

- Ensure transparent communication regarding subscription terms and cancellation policies.

- Send confirmation emails for orders and shipping updates to keep customers informed.

- Invest in fraud prevention technologies.

Impact on High-Risk Merchant Accounts

Chargebacks can significantly impact high-risk merchant accounts due to the higher likelihood of disputes. Too many chargebacks may lead to higher processing fees and even termination of merchant services, making it crucial for these merchants to monitor chargeback rates and address issues proactively.

FAQs on Chargeback Reason Codes

Discover essential questions related to chargebacks.

What should I do when I receive a chargeback?

Review the chargeback reason code and gather evidence to dispute the chargeback if necessary.

How can I prevent chargebacks?

Ensure clear product descriptions, maintain communication with customers, and use fraud protection tools.

What happens if my chargeback ratio is high?

A high chargeback ratio can lead to increased fees or termination of your merchant account.

Can products be returned instead of filing a chargeback?

Yes, customers should contact merchants for returns before resorting to chargebacks.

How long do I have to respond to a chargeback?

Typically, merchants have 30 days to respond, but this may vary by card network.

Do chargebacks affect my credit score?

Chargebacks do not directly affect credit scores but may impact merchant account standing.

Ready to Manage Your Chargebacks?

Don’t let chargebacks impact your business. Apply now for expert assistance.

Apply Now →